Money - A Prolegomena

Money, a crucial pillar of modern economies, is often overlooked by mainstream economics. This critical introduction, a prolegomena, lays out the fundamentals of how our modern economies operate.

Money, a crucial pillar of modern economies, is often overlooked by mainstream economics. This critical introduction, a prolegomena, lays out the fundamentals of how our modern economies operate.

"Philosophy is a battle against the bewitchment of our intelligence by means of language." - Ludwig Wittgenstein, Philosophical Investigations §109

Money is a cornerstone of modern economies, yet political economy is a battle against the bewitchment of our intelligence by means of myths and misconceptions. Many still believe that banks lend out other people’s savings, that governments create most of the money supply, or that money must be backed by gold or silver.

We cannot influence properly that which we don't understand.

Our societies face a democratic deficit because we lack the political will to make the necessary reforms for ensuring finance works for the polity. Underpinning this lack of will is institutional capture and a lack of understanding among the populace about how finance actually works.

What is the most potent delusion we hold about money? That it is an object.

When we think abstractly, our cognition is shaped by the concrete world around us—a phenomenon psychologists call embodied cognition. For example, lifting a heavier object can make us associate it with greater importance. Similarly, we perceive coins or metal as more valuable because they feel substantial or look luxurious—an effect known as the endowment effect.

This helps explain our preference for physical money over digital forms. Even a plastic debit card feels more “real” than the intangible numbers in a phone app.

Construal level theory deepens this point: we trust what feels closer to us. Physical currency is immediate and familiar. Institutions, by contrast, feel distant—and thus less trustworthy.

Historically, this bias toward tangibility shaped early money. Shells were used by traders because they were rare and beautiful. The Sumerians used barley and silver, and coined the term shekel—from the Akkadian 𒂅 šiqlu, meaning “weight.” This seems to support the idea that money began as a commodity, a theory known as metallism.

But money is not an object.

Gold, silver, and salt are commodities. They are not money today. Gold is sold on commodity markets; salt is a supermarket good. Shells are fragile and common. Even gold coins must be minted before they circulate as money—and those coins are now antiques, valued for their historical worth, not their monetary function.

Money is a social technology, a tool we developed to solve civilisational problems that would otherwise remain intractable, as argued by anthropologist Mikael Fauvelle (2024:10). Social cohesion, order, and trade require relationships—and, critically, trust.

In large societies, individuals must keep track of obligations, roles, and promises—even between people who are not kin, who may rarely interact, or whose dealings stretch over years. Without such organisation, advanced civilisations—like those of ancient Mesopotamia—would be impossible.

This all results from what economists call the division of labour - the specialisation of labour activity towards specific activities. Initially men may be both gatherers of food and warrior. However, an elderly person displaying much wisdom isn't useful hunting boars or fighting invaders or invading others. As societies become more complex, gathering food and fighting become specialised roles. Warriors end up choosing between infantry and calvary. Food gatherers start specialising in gathering particular types of food, whether barley or raw meat. Markets are created so these goods can be sold to the warrior. Over time, this results in what Adam Smith called the 'commercial society'. Ironically, Smith got the origins of money entirely wrong. The purpose of finance is creating markets and specialisations that never existed before and which resources need introducing.

Money helps resolve problems like:

In his pioneering work Outlines on the Origin of Money, Heinrich Schurtz introduced the important distinction:

This distinction still matters. Most dollars today are created outside the U.S., in the Eurodollar market. But is a Eurodollar inside or outside money?

It depends. For the U.S. Treasury, Eurodollars are outside money—they exist beyond domestic control. But for international banks trading among themselves, they function as inside money within their own network of obligations.

Credit is a social technology that defers final payment. But its deeper function lies in creating mutual obligations within a society. The deferral of enforcing obligations—including repayment—is how credit operates, not what it is. At its core, credit is an IOU: "I owe you."

A creditor extends funds under specific terms; the debtor accepts the obligation to repay. The creditor holds the IOU as a claim, while the debtor recognises it as a liability. This claim includes repayment conditions and interest—compensation for the initial outlay.

The word credit comes from the Latin credit, meaning “one believes.” Trust is foundational. Without it, credit collapses, and the social and economic ties it enables unravel. Credit is a mechanism for trust-building, encouraging obligations that bind individuals to one another. Strong institutions magnify this process, accelerating economic development.

In early human societies, credit was often the default mode of exchange. Reciprocity governed such economies: the IOU implies a UOI—"you owe I." I give you ten chickens today; you owe me a cow in a month. Violating such obligations could mean social expulsion—often a death sentence in tightly interdependent communities. In these systems, mutuality was essential for survival and free-riding intolerable.

Credit provides flexibility. It lets people access goods or services now, while paying later when resources become available. Payments could take the form of crops, labour, or luxury goods - whatever the creditor found valuable. In more coercive settings, the debtor could become the payment—laying the groundwork for slavery as both a social relation and a brutal technology of control.

Economists, historians, and anthropologists disagree on what ultimately caused the emergence of money. Given the scant and scattered evidence from ancient times, we're asking the wrong question. Instead of looking for a singular origin, we should see money as a social technology that enabled more complex relationships and the development of civilisation itself. The way different societies developed money reveals more about their particular histories than about any universal origin.

We should ask instead:

From at least 100,000 years ago, ancient economies were gift- or credit-based. German ethnologist Heinrich Schurtz observed that there is no evidence of barter economies. Archaeologist Michael Hudson highlights how Mesopotamian evidence links money closely to credit, debt, and mutual obligations.

In pure credit economies, unresolved obligations become a social, economic, and political burden. An excess of obligations can impoverish the population and, in doing so, delegitimise the sovereign. This raises difficult political questions: Who should be free, and who should be enslaved? Who belongs to the polity, and who does not? How can we discharge obligations in a way that preserves social stability—and at what cost?

Cambridge CoreMikael Fauvelle

Cambridge CoreMikael Fauvelle

Anthropological archaeologist Mikael Fauvelle specialises in investigating economic and political complexity in pre-state and non-state societies. In his recently published Shell Money: A Comparative Study, he argues that money predates sovereign authority. In pre-state hunter-gatherer societies in Southern California, shell beads served as money, thereby facilitating trade among strangers and across boundaries long before the emergence of formal political structures. This pattern emerges not just in south California but throughout the world. The evidence suggests trade is essential for establishing money.

Money, in this context, is not born of state decree but private necessity. Trade requires a medium of exchange. Whether the actors involved are private individuals or tribal leaders acting on behalf of their communities, trade across social boundaries demands a trusted, recognisable unit of value. As civilisations became more complex, internal trade intensified and pure gift or credit economies—based on mutual obligation and reciprocity—became insufficient.

For trade across tribes or distant communities to function, participants needed a mutually recognised standard of payment. Scarce and valuable commodities such as shells, beads, or metals—often tied to prestige—came to fill this role. A trader would not accept a gift or obligation from someone they did not know; but they might accept a commodity recognised as valuable by all.

This necessitated new forms of political organisation. Internally, societies required institutions and norms to regulate trade and coordinate complexity. Externally, scarce and recognisable money enabled long-distance commerce. In regions like Mesopotamia, where critical resources were often lacking, such trade was essential for survival. Thus, money enabled—not followed—the rise of the sovereign and the state. The state is the creature of money, not its master.

Why did money beget the state rather than the reverse? Because money builds trust. Credit and money facilitate relationships based on deferred and mutual recognition of obligations. Sovereignty, by contrast, imposes authority. While authority can regulate trust, it does not inherently generate it. Still, states were critical in codifying and standardising the norms surrounding money, giving it institutional backing as societies scaled.

Tribal societies did not require sovereigns because interpersonal ties were sufficient to maintain order. Leadership existed, but it was embedded in proximity and mutual recognition—typically the wisdom of an elder. But as societies grew in scale and complexity, they required social technologies like law—and money—to function smoothly.

Even though money preceded the state, there is a close relationship between the emergence of money and sovereigns. Trust remains the foundation. The strength of metallic money lies in its ability to preserve trust where institutional or interpersonal trust is fragile. People might not trust a foreign ruler, but they might trust gold.

This becomes especially relevant in imperial contexts. Why would a citizen of the Sasanian Empire trust the authority of the Byzantine Emperor? Acceptance of a foreign currency signaled tacit consent to the issuing sovereign’s domain. When a sovereign could not regulate distant subjects directly, coins became a symbolic projection of authority—an expression of imperium.

In the modern age, sovereigns no longer require physical tokens of metal to project their power. Within functional states, authority is institutionally embedded and geographically secured. Today’s fiat money—money with no intrinsic commodity value—is sustained by trust in state and banking institutions. But the principle remains: money flows from trust, and trust enables money.

"Money therefore only comes into existence once a payment is made" [Graziani 1990, p.11].

Another persistent myth blights our understanding of money: that there is a fundamental, clear-cut distinction between money and credit. In reality, the two are not only interrelated—they are often indistinguishable. Central bank currency is money to citizens, but credit for the central bank and the state. Bank deposits are money for customers, but represent liabilities—credit—for the banks themselves. Securities can function as money for those willing to accept them in payment, but remain mere credit instruments for those who don’t.

What's money for you is credit for someone else. This is the essential fact of the modern economy. Money and credit are both IOU's. Whether an IOU is credit or money is determined by who you are relative to the rest of the economy, the time you use an IOU, and the function by which you use the IOU. During bank runs, it becomes clear that bank deposits are forms of credit to the banks customers and that the bank may not pay out.

Still skeptical? Consider the inscription on every pound sterling note:

I promise to pay the bearer on demand the sum of X pounds

The Bank of England distributes banknotes, i.e. IOU's, throughout the economy. It is a promise that the IOU represents the sum on the note and that the note can be exchanged for notes of equivalent value. Two factors allow this to occur. First, we implicitly trust that the Bank of England will keep its promise. In modern times, this is done through institutional design and monetary policy, though neither are without significant flaws. Second, the authority of the state ensures such notes must be accepted as means of paying off debts. This is what's called legal tender. Legal tender doesn't mean that shopping outlets must accept banknotes, but rather that creditors must accept these banknotes as payment by the debtor according to the value of the sum on the notes.

This is a promissory note, an IOU issued by the Bank of England. It circulates as money because the public believes in two things:

Legal tender status does not mean shops must accept cash—they can set their own payment policies. Rather, it means that, legally, a creditor cannot refuse banknotes as payment for a debt. If the state revoked this status, or the central bank broke its promise, trust would unravel. Imagine if £50 notes were suddenly redeemable only for £5. Or if hyperinflation rendered the notes worthless. These hypothetical breaches would turn money into the decorative paper they really are in a fiat money system.

While such breakdowns are unthinkable in the UK at present, they are not mere thought experiments globally. (Some may even argue that former Prime Minister Liz Truss’s budget crisis revealed that the UK is not immune to a sudden loss of trust.) The fragility of monetary confidence becomes especially clear in foreign contexts. Outside the UK, a pound sterling note is meaningless—unless you’re a forex trader. A café in Paris or a vendor in Warsaw won’t accept pounds. Why would they? They’d incur a loss converting them, and no legal or institutional framework obliges them to accept it.

The value of money, therefore, is not intrinsic. It is relational, institutional, and above all—political. Just as the state was once a creature of money, so modern money is now the creature of the modern state.

Balance sheets—also known as Godley tables—are an analytical tool for recording financial transactions. While companies and financial institutions are legally required to maintain accurate balance sheets for regulatory and accounting purposes, our interest lies in something deeper: using them as a means of thinking rigorously to understand how banking, finance, and financial systems actually function.

Why should we care about the swap? Because understanding the financial system requires understanding how payments are actually made. And payments, at their core, are settled through the clearing system. Godley tables are indispensable for tracing these exchanges—between individuals, firms, and institutions—so we can clearly see what’s happening behind the scenes.

A Godley table consists of two columns:

Take, for instance, Figure 1 from Young (1999, p.308), which presents the balance sheet of the Bank of England’s Issues Department. On the asset side, we find £126,234,595 in Gold Coin and Bullion. This is outside money—a form of money treated as an asset by everyone: the central bank, commercial banks, the private sector, and individuals alike. No one holds gold as a liability.

On the liability side, however, we see £145,984,595 in Notes issued. These are inside money. While the public and private sector regard these notes as assets, the Bank of England sees them as liabilities—claims it must honour. The distinction between inside and outside money is crucial: it helps us map where trust, credit, and obligation reside within the monetary system.

There are two key things to note:

Every financial transaction in the modern economy is a swap of IOUs—a promise to pay someone 'I owe you'. Financial activity predominantly involves swapping, i.e. exchanging, IOUs. The swap is the fundamental instrument underpinning all exchanges. To think rigorously about finance and monetary economics is to think in balance sheets.

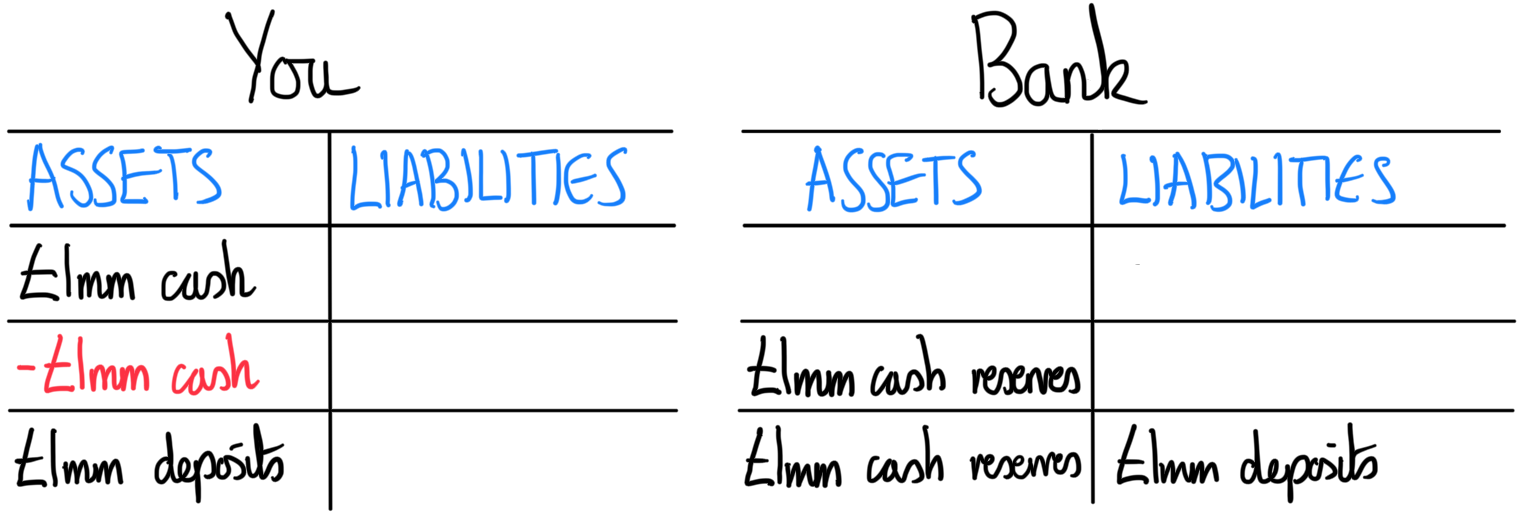

Let’s consider a simple example: depositing £1 million in cash at a bank.

Here’s what happens:

At no point does the bank merely place the cash in a vault for safekeeping. It takes the cash as reserves and creates a deposit account of equal value.

By the end of this transaction:

Now let’s use this £1 million deposit to obtain a £10 million loan from the same bank.

The first line merely tells us what we already know, that we've deposited £1mm in cash to the bank.

Bank of England home

Bank of England homeIn line 2, the bank creates the loan. This expands both your balance sheet and the bank’s. On the bank’s side, the loan is an asset—it expects repayment—and the newly created deposit is a liability. On your side, the deposit is an asset, while the loan is a liability you will need to repay.

The deposit and the loan are simultaneously created by the bank. Neither existed before. Neither existed prior to this transaction. Through this action, the bank has created new purchasing power—it has literally generated money where none existed before. We call this endogenous money creation. This is the essence of how money is not merely transferred, but created through the process of lending.

Private banks create the vast majority of money through demand deposits when they issue loans. This process generates new purchasing power without reducing anyone else’s. In doing so, banks create a circuit: a flow of money and credit that continues until someone repays the debt or settles a tax obligation, effectively destroying that money and closing the loop.

Private banks create the overwhelming majority of money through demand deposits when loans are issued. They generate new purchasing power without diminishing anyone else’s—a fundamental feature of the banking system. This process sets in motion a circuit of money and credit, which traces the flow of new purchasing power throughout the economy until it is ultimately destroyed. This framework is called monetary circuit theory, or circuitism for short.

Bank of England homeThere are important constraints to this process of creating money:

With this newly created purchasing power, you invest £10 million into the Green Hydrogen Enterprise.

The Green Hydrogen Enterprise begins with £100 million in equity. It sells £10 million of that equity to you in exchange for bank deposits. You now hold £10 million in equity—an asset that may generate profit and help you repay the loan. The bank has simply transferred the deposit from your name to the firm’s account.

This example is simplified: we’ve assumed both parties use the same bank. If they didn’t, the bank might need to transfer reserves to another institution—or even borrow reserves on the interbank market. In reality, financial transactions are far more complex. Even everyday actions, like dining out with a credit card, involve similar underlying mechanics.

Monetary realism pushes back—not with ideology, but with observation. Money is real, it matters, and it shapes everything. If we want to understand the economy, we have to study how money actually works in practice—not in theory, not in abstraction, but in the real world.

Ignoring or abstracting away from money—as neoclassical economics tends to do—hinders our understanding of the economy. Money is not a mere veil that hides the true nature of exchange. Banks are not intermediaries simply facilitating payment; they create markets. Finance serves to defer the funding of present investments for the real productive economy—at least, that's how it should work.

However, finance becomes self-indulgent. Rentier speculation—profiteering purely for the sake of profiteering by manipulating resources—can become more important than making tangible material progress that improves people's lives. Without proper understanding of the economy, we cannot shape it to ensure that productive activity genuinely helps people live fulfilling lives.

"Ipsa scientia potestas est." – Francis Bacon.

Monetary realism is not a doctrine about what money is, but a method for analysing the economy. Money is a social technology, and like all technologies, innovations occur. Over time, these innovations can become so profound that previous paradigms become irrelevant.

Perry Mehrling, in his course The Economics of Money and Banking, states that there are four prices of money in the economy. We cannot be monetary realists ignoring or downplaying the significance of each price of money.

All money in a given denomination should be priced the same. £5 in banknotes should be equivalent to £5 in bank deposits. There should be no difference between the price of currency and the price of a demand deposit. Monetary economists refer to this as the price of par – the price of money in terms of other money, e.g., the price of a unit of currency is the same to that of a unit in a demand deposit account at a bank.

Par is vital for the stability of monetary systems. I cannot trust a money system if I don’t know whether I could gain or lose money simply by exchanging money with others. Without par, I cannot trust. The power of par is that we can treat demand deposits from a bank as if they were currency.

During financial crises, when the system is under strain, par can cease to exist. For instance, during a bank run, people panic, fearing they won’t be able to retrieve all the money in their deposit accounts, so they demand their deposits be converted to currency. If the conversion isn’t possible, e.g., £1 million in deposits only yields £75k in currency, then par no longer holds. Without par, banking would be impossible, and sophisticated financial systems would be unfeasible and non-functional.

Interest is the price of money in terms of future money, effectively acting as the cost of deferring payment.

Interest is deeply embedded in modern economies, so much so that it has become systemic. By having a price of money tied to future money, economic growth is incentivised, even if such growth is unsustainable in the long term.

Paying interest requires not only earning money to repay a debt but also meeting the additional burden of interest payments. Both individuals and businesses must generate a profit to cover their debt obligations.

The earlier example of investing in the Green Energy Enterprise should illustrate why. If you only broke even by investing, then you couldn't use the surplus from the investment funding the loan.

This is true in the housing market where increasing house prices is necessary so people remain solvent while paying off the interest of the mortgage.

The imperative to remain solvent and meet interest obligations compels both states and firms to pursue growth at any cost. Often, this means extracting and burning carbon-intensive resources to sustain revenue flows. The result is a self-reinforcing cycle of debt-driven expansion that accelerates ecological breakdown and contributes to the ongoing collapse of Earth’s biodiversity.

Bernard Lietaer discusses this in the talk below. Nevertheless, creating purchasing power is a powerful tool for spurring economic development and progress.

Bernard Lietaer giving a presentation about monetary reforms allowing for a more sustainable economy

Exchange rates represent the price of money in terms of other currencies, e.g., the value of the pound sterling (£) in relation to the US dollar ($). This is the domain of foreign exchange (forex) markets.

Exchange rates affect how individuals, organisations, and states buy and sell goods internationally. A favourable exchange rate can make trade cheaper, stimulating economic activity, while an unfavourable rate can make trade more expensive, discouraging it. Highly volatile exchange markets are beneficial for short-term speculative trading but detrimental for those seeking stable, long-term trade relationships.

Central banks will buy and sell foreign reserve currencies to influence the forex markets, maintaining domestic price stability. Such actions, though purposeful, should be subtle, ensuring that stability is achieved without disrupting the natural flow of economic forces.

The price-level is the price of money in terms of commodities. For example, how many pounds sterling do I need to buy an apple? This is the realm of inflation and deflation. Inflation increases the price level nominally. If purchasing power does not increase to keep up with inflation, people become poorer because the real cost of commodities has increased. If purchasing power outpaces inflation, then despite inflation, people are richer.

Deflation, the decline in the nominal value of commodities, can be especially harmful to the highly indebted. As asset values fall while liabilities remain the same, economic actors can become insolvent. However, deflation does make commodities cheaper.

Central banks manipulate interest rates as a means of promoting or inhibiting demand for credit, thereby influencing the price level. Furthermore, central banks' influence over foreign exchange (forex) markets also plays a role, particularly in countries that rely heavily on trade for core commodities such as food and energy.

Few concepts in modern monetary economics are more revealing than Perry Mehrling’s Hierarchy of Money.

At its core, the monetary world is hierarchical. Money is an IOU—a promise to settle a payment. But not all promises are equal. Who decides whether a payment has truly been settled? In theory, everyone does. In practice, some promises carry more weight than others. Some actors issue promises the market trusts more than others. Some money is better than other money.

During financial booms, private securities may be treated as money. People accept them as settlement because they believe they can easily resell them—often at a profit. We call this liquidity. The more liquid an asset is, the more readily it can be exchanged.

In periods of confidence, even speculative securities can function as money. But when the bubble bursts, trust evaporates and people seek money that's higher up in the hierarchy, whether they be deposits, currency, or central bank reserves. Those same securities become recognised for what they are—credit, not cash. The willingness to accept them disappears.

This reveals a deeper truth: whether a form of credit becomes money depends on trust, where you are situated in the hierarchy of money, market dynamics, and liquidity. The more secure and trusted the IOU, the closer it is to functioning as true money. In prosperous times, the boundary between money and credit blurs. "Money is credit. Credit is money." But this is only true under optimistic conditions—the so-called animal spirits of financial markets.

In more cautious or “sober” periods, distinctions resurface. Markets only treat secure, credible credit as money. Some IOUs are too risky to be trusted as means of payment. The hierarchy becomes visible again.

In times of crisis, the split becomes undeniable. Central banks issue the highest form of money in the system—cash and reserves backed by state power and institutional trust. Meanwhile, bank deposits—normally treated as money—can lose credibility. We realise they are, in fact, private promises. If those promises are doubted, they’re treated as what they really are: unsecured credit.

At par, £1,000 in a deposit should equal £1,000 in cash. But under stress, this equivalence breaks down. We trust the Bank of England more than we trust Barclays. We trust Barclays more than we trust hedge funds or crypto platforms. This qualitative difference—how trustworthy the issuer is—forms the basis of the hierarchy of money.

Some money is more trustworthy than other money. Some credit is more credible than other credit. This is not just a technicality—it shapes how the monetary system functions in practice. At the top sit central bank reserves and currency, the most secure forms of money. Below that are commercial bank deposits, then money market instruments, and further down, various types of private credit. The system is layered—each layer relying on the credibility of the one above. This layered system doesn't just affect institutions—it shapes everyday behaviour, especially in how people choose which money to spend or save.

Crucially, the best money is scarce, and the worst money is abundant. 'Notes and coin' represent a small fraction of the UK money supply. Central bank reserves are limited and used mostly between financial institutions. Yet commercial bank deposits—less secure, privately issued—make up the vast majority (around 96%) of the money in circulation. The hierarchy isn’t just conceptual—it’s structural.

This reality is captured in Gresham’s Law, which states that "bad money drives out good money." When two forms of money circulate at the same nominal value but differ in perceived quality, people hoard the ‘good’ and spend the ‘bad.’ Why hand over something you trust when you can get rid of something you don’t? The result: high-quality money vanishes from circulation while the lower-quality money remains.

Gresham’s Law reflects the hierarchy in motion. If a system flooded itself with only good money, it would debase that money’s quality—often through inflation, eroding its real value. This would be true even if there was no increase in the money supply. This interplay of trust, liquidity, and hierarchy shapes the entire monetary system. Money, at its core, is not just a number. It is a claim, and the credibility of that claim depends on who is making the promise. And that credibility—the invisible architecture of finance—is what holds the entire system together, or lets it collapse.

If the four prices of money and the monetary hierarchy describe the structure of the system, then flux and reflux describe its dynamics. In any monetary system, the movement of money unfolds through a dynamic interplay between initial financing and final financing as Auguste Graziani termed them. Perry Mehrling refers to these processes as flux and reflux, or funding.

Initial financing (flux) is the creation of purchasing power—it involves the issuance of IOUs that expand the money circuit. This is when credit is created and injected into the economy, allowing actors to act. Funding (reflux), by contrast, is the process of extinguishing those IOUs, either through repayment or through conversion into higher-quality IOUs, such as money. Flux expands; reflux contracts. Both are mechanisms of payment.

This logic applies to both public and private finance. In public finance, initial financing occurs when the state spends money into existence—creating purchasing power through expenditure. Funding, in this context, involves withdrawing money through taxation or the issuance of bonds. The state first spends, then funds—expenditure precedes revenue.

But note: one actor’s initial financing can be another’s funding. Your purchase of equity was flux from your perspective, but for the firm issuing the equity, it was reflux—they were funded. With that funding, the firm could invest in clean technology, generate profit, and allow the cycle to continue. The circuit relies on a continuous rhythm of flux and reflux—creation and redemption.

If flux and reflux describe the motion of money—its expansion and contraction—then elasticity and discipline describe the forces that shape that motion. They are the underlying tendencies that push a monetary system toward either greater creation (flux) or greater settlement of payment (reflux).

Elasticity is the system’s capacity to expand credit and purchasing power when needed. It reflects a willingness to create IOUs and accommodate new spending. When elasticity is too low, credit is scarce, demand is suppressed, and the economy suffers under the weight of its own inertia. But too much elasticity, and the system becomes dangerously loose: credit grows beyond the productive capacity of the economy, leading to inflationary pressures or the mispricing of risk—what Hyman Minsky called financial fragility. Central banks typically respond by adding discipline to the system by increasing interest rates restricting demand for credit creation by incurring greater costs onto it.

Discipline, by contrast, is the system’s ability to enforce repayment, to compel reflux. It ensures that IOUs are not only created, but honoured. When discipline is excessive, it suppresses economic activity, favouring deleveraging over investment. This is the terrain of debt deflation, where efforts to repay debts contract the money supply faster than debt itself is reduced. There is too little liquidity in the system. Central banks typically 'loosen' monetary policy by making it easier for private sector agents to lend creating elasticity in the system.

Elasticity and discipline are very much like yin and yang within the monetary system. One expands, the other constrains. One fuels growth, the other preserves solvency. Markets oscillate between the two, and a stable monetary system must strike a balance between them. When either force dominates for too long, the result is instability—boom, bust, or both in sequence.

Understanding elasticity and discipline as systemic forces reveals that monetary stability is not about targeting a fixed supply of money. It’s about managing a dynamic, evolving hierarchy of promises—ensuring the right balance of creation and redemption, optimism and caution, flux and reflux.

The historical debate between Chartalism and Metallism lies at the heart of our understanding of money’s nature—whether it derives value from the state or from commodities.

Metallism holds that the value of money is derived from its link to a commodity, typically gold or silver. Under a gold standard, for example, money is pegged to a specific quantity of gold; under a silver standard, to silver. For most of history, societies operated with commodity money: sometimes directly—as with shells, salt, or minted gold coins—or indirectly, by pegging their currency’s value to a metallic anchor.

Chartalism, by contrast, asserts that the value of money stems from the sovereign’s authority. A state gives its currency value by demanding taxes be paid in it, creating demand for the currency. Legal tender laws reinforce this by compelling its use in settling debts. Moreover, the sovereign decides which commodity, if any, shall serve as monetary backing—and at what rate. Even under metallic regimes, it is the state that declares which metal holds primacy and sets its exchange ratio.

Today, Metallism is empirically false. No modern economy backs its currency with gold or silver. All major currencies are fiat—backed not by metal, but by trust in the authority that issues them, typically the central bank and treasury.

Does this mean Chartalism is true? Not entirely. While modern systems are Chartalist in structure, most money is not created by the state, but by private banks—upwards of 96% of the money supply. Banks extend credit by issuing deposits, denominated in the sovereign’s currency and exchangeable at par. Their capacity to do so, however, is licensed and regulated by the state.

As Perry Mehrling aptly argues, the system is hybrid. It is neither wholly Chartalist nor Metallist, neither purely public nor purely private. It reflects a monetary duality, in which the sovereign sets the rules of the game while private actors generate most of the plays. We live in a fiat-chartalist regime, but one layered with privately created money operating under market incentives.

In the hierarchy of money, the sovereign's currency remains supreme. This is evident through phenomena like Gresham’s Law: in a system of multiple forms of money, “bad” (or lesser) money drives out “good” money in circulation. Bank deposits are not equal to physical currency in safety or liquidity. If all depositors demanded cash simultaneously, the system would falter. This reveals that state-backed currency is the ultimate domestic settlement asset.

Nonetheless, the central bank, while powerful, is not omnipotent. It nudges rather than commands. Its primary tool is interest rate policy, through which it influences—rather than dictates—the elasticity and discipline of private money creation. The central bank uses monetary policy as a means of influencing the forces of elasticity and discipline keeping them in balance. Yet markets influence central banks as much as central banks influence markets. The relationship is dialectical.

Chartalism certainly describes key facets of today's modern monetary systems. Governments determine what is legal tender and imposes taxes on the populace. However, on top of that is a vast layer of privately issued money with a life of its own.

This brings us to the yin and yang at the heart of monetary governance: a public-private hybridity. Both the state and the market play constitutive roles. The boundary between them is not fixed, but negotiated and dynamic. Sometimes markets overpower the state—such as in financial bubbles or capital outflows. At other times, the state imposes its will—such as during wartime finance or crisis bailouts. Where one sees liberty, another sees instability; where one sees authority, another sees repression.

A historical example makes this concrete. As Allyn Young observed in his essays The Mystery of Money and The Monetary System of the United States, America’s monetary history is a study in the tension between state decree and market reaction.

In 1792, President George Washington signed the Coinage Act, authored by Alexander Hamilton, which established the U.S. Mint and formalised the dollar as the nation's currency. The Act created a bimetallic standard, fixing the ratio of silver to gold at 15:1 and pegging the dollar to the Spanish silver dollar. Coins were issued in copper, silver, and gold—valued by the state and minted by public authority.

Yet the market undermined the system almost immediately. Gold’s market value shifted, moving the true ratio closer to 15.5:1. As a result, gold was undervalued and vanished from circulation, while silver flooded the system. Subsequent legislation adjusted the ratio to 16:1, eventually phasing out silver for large payments. By 1853, silver was legal tender only for small transactions.

As Allyn Young notes, the silver standard was an endorsement of cheap money. Creditors favoured gold-backed money because the value of debts rose, whereas debtors preferred the cheap money of the silver standard.

The episode reveals a core lesson: sovereign authority can decree, but it cannot dictate market behaviour. Even with legal power, the state found its coinage policy misaligned with market prices, leading to practical failure. Despite the intent of the 1792 Act, the U.S. never had a robust gold currency in circulation—until later acts recalibrated the system.

The broader insight is that economic liberty constrains state power, just as state authority limits market excess. Sovereignty is not absolute. The state can shape conditions, but it cannot escape the consequences of those conditions. Monetary regimes, like societies themselves, are fragile equilibriums—a constant negotiation between order and freedom.

Thus, in choosing a monetary system, we are not merely selecting a technical apparatus—we are deciding the balance of power between public and private forces, between state and citizen, between decree, demand, and liberty. Economic liberty constrains the state's authority empowering market forces, however the constraints imposed still give the state liberty in influencing the market. When states decree what the nature of their monetary regime is, it has a direct impact on how free citizens are in that's states economy. More control is not necessarily good, for instance debtors didn't benefit from the moves towards gold. Meanwhile, unfettered markets and private desire destabilise the system emphasising private interests over the public good.

This balance cannot be established through force of will. Radical action, if it is to be wise, must arise through the subtle transformation of the roots of imbalance, allowing a new harmony to emerge of its own accord. Unwise radicalism merely deepens disorder, addressing symptoms while leaving the causes untouched. This is precisely why we must understand money.

The constancy of the course lies in doing nothing

yet leave nothing undone [無為而無不為]

If lords and kings could hold fast to it,

all things would transform of their own accord

- Laozi in the Daodejing §37

Fauvelle, M. (2024) Shell Money: A Comparative Study. Cambridge: Cambridge University Press (Elements in Ancient and Pre-modern Economies).

Graziani, A. 1990. The Monetary Theory of Production. Cambridge: Cambridge University Press

Laozi. Trans: Ziporyn, B. 2024. Daodejing. New York: Liveright

Mcleay, M., Radia A., and Thomas, R. 2014. Money in the modern economy: an introduction. Quarterly Bulletin 2014 Q1. Bank of England

Mcleay, M., Radia A., and Thomas, R. 2014. Money creation in the modern economy. Quarterly Bulletin 2014 Q1. Bank of England

Mehrling, P. Economics of Money and Banking. Coursera

Mehrling, P. 2012. The Inherent Hierarchy of Money. Source: https://sites.bu.edu/perry/files/2019/04/Mehrling_P_FESeminar_Sp12-02.pdf

Young, A. Mehrling, P.G., & Sandilands, R.J. (Eds.). (1999). Money and Growth: Selected Papers of Allyn Abbott Young (1st ed.). Routledge.